THE BANKING INDUSTRY CONSOLIDATION CONTINUES BELOW HISTORICAL AVERAGES.

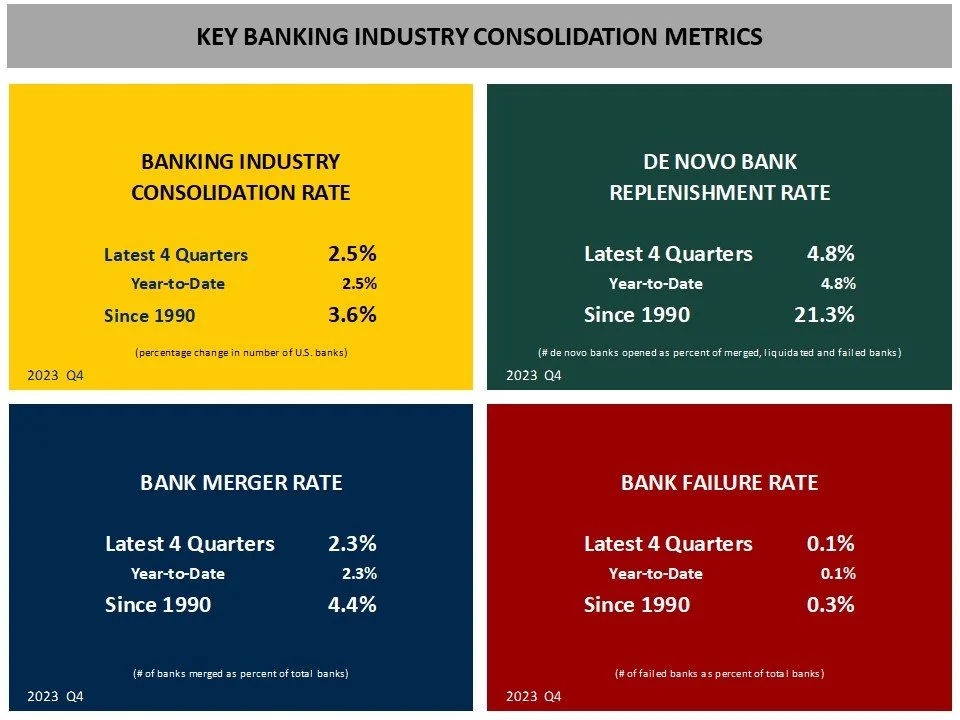

Banking Industry Consolidation Rate = 2.5% for L4Q. The pace of industry consolidation was well below the historical average since 1990 of 3.6%. The industry is entering its fourth year of below average consolidation.

Bank Merger Rate = 2.3% for L4Q. The pace of bank merger activity was well below the historical average since 1990 of 4.4%. 2nd lowest merger rate in last three decades.

Bank Failure Rate = 0.1% for L4Q with 6 bank failures , including three larger banks suffering depositor runs. The historical average since 1990 is 0.3%.

De Novo Bank Replenishment Rate = 4.8% for L4Q - even with such low merger activity. The replenishment rate was well below the historical average since 1990 of 21.3%.

NUMBER OF U.S. BANKS:

Overall, the number of U.S. banks fell to 4,587 at the end of Q4 2023 - down 119 from one year ago.

The largest declines continued to occur in Community Banks with less than $500 million in total assets.

And the largest declines of headquartered banks continues to occur in rural markets with populations of less than 50 thousand.

BANKING INDUSTRY CONSOLIDATION RATE:

Banking industry consolidation net activity slowed during 2023 Q4 L4Q. The Banking Industry Consolidation Rate for 2023 was 2.5%. The historical average was 3.6% since 1990.

Community banks consolidated at a rate of 2.6% L4Q with several states showing a consolidation rate of 4% or higher: Florida, Illinois, Wisconsin, and Pennsylvania.

BANK MERGER RATE:

Bank merger activity slowed significantly for the L4Q through Q4 2023. The Bank Merger Rate was 2.3% - 2nd lowest merger rate in three decades. The historical average was 4.4% since 1990.

DE NOVO BANK REPLENISHMENT RATE:

De novo banking activity remains historically low with 6 new banks opened during the L4Q through Q4 2023. The De Novo Bank Replenishment Rate was 4.8%, or approximately 5 new banks opened to replace every 100 banks lost to merger, failure or liquidation. This rate remains well below the historical average or 21.3%, or 21 new banks opened to replace every 100 banks lost to merger, failure or liquidation.

BANK FAILURE RATE:

There were six (6) bank failures for the L4Q ending Q4 2023. The Bank Failure Rate was 0.1%.

Three (3) of these bank failures were the result of large, uninsured depositor runs resulting from a loss of confidence caused by significant losses in the AFS and HTM securities portfolios. Also, a small community bank - $140 million in Total assets - failed as a result of a $47 million crypto scam.

Financially, the industry is sound. Earnings were solid. Credit quality continues to look good. And capital levels remain strong.

2024 OUTLOOK: SLOWER CONSOLIDATION

The pace of banking industry consolidation is expected to continue below historic averages.

This pace will result from a below average rate for bank mergers. There is no reason to believe that any unusual resurgence will occur.

The bank failure rate should continue to remain near zero during 2024.

And de novo bank activity will continue at less than 10 per year with the de novo bank replenishment rate in the 5% range or less.