The banking industry consolidation continued into Q1 2022, matching historical averages.

Banking Industry Consolidation Rate = 3.7% for the latest 4 quarters (L4Q), matching the long term annual rate of 3.7%.

Bank Merger Rate = 3.7% L4Q, below the 4.5% rate of the past 3+ decades.

Bank Failure Rate = 0.0% with no failures L4Q, showing the financial strength of the industry today.

De Novo Bank Replenishment Rate = 4.7% L4Q - remaining low and significantly below the average rate of 21.0% over the past several decades.

BANK CHARTERS:

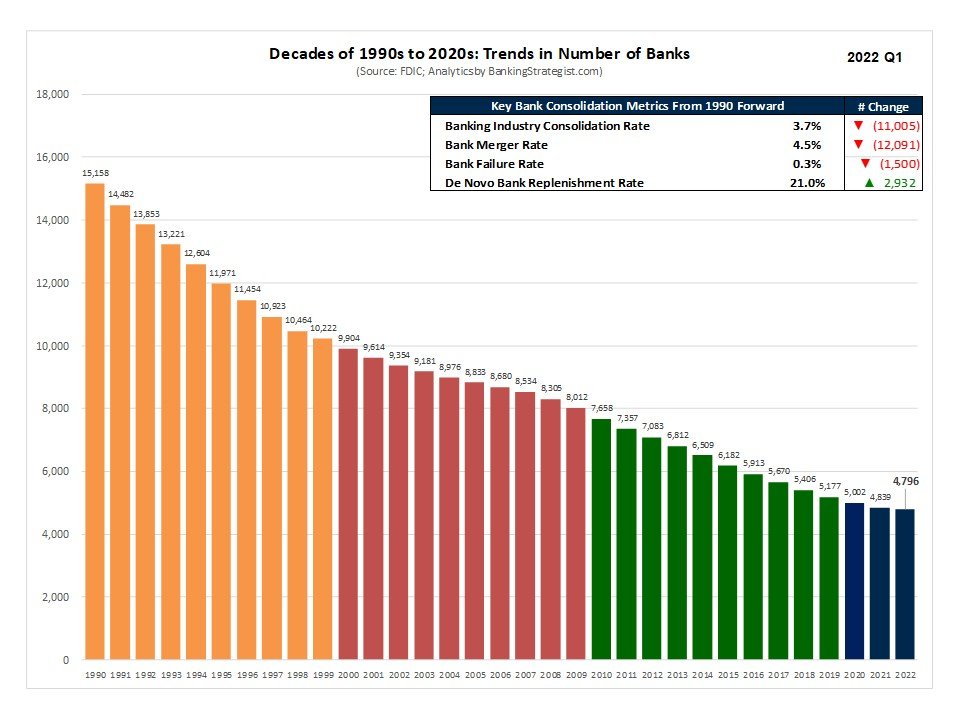

Overall, the number of banks in the U.S. fell to 4,796 at the end of Q1 2022 - down 182 from one year ago.

The largest declines occurred in Community Banks with less than $250 million in total assets.

And, importantly, the largest declines occurred in rural markets with populations of less than 50 thousand.

BANKING INDUSTRY CONSOLIDATION RATE:

The rate of banking industry consolidation matched the historical average of 3.7%.

For the L4Q, the Banking Industry Consolidation Rate was 3.7%, or approximately 37 banking charters disappeared for each 1,000 banks existing one year ago.

Community Banks consolidated at a rate of 3.8% L4Q with several states showing a consolidation rate of greater than 4%: Missouri, California, Illinois, Texas, Iowa, Minnesota, Oklahoma, and Alabama.

BANK MERGER RATE:

Bank merger activity picked up during the first quarter of 2022. The Bank Merger Rate was 3.6% compared to an average rate of 4.5% since 1990 and above the 3.3% rate during 2021.

DE NOVO BANK REPLENISHMENT RATE:

While de novo banking activity has seen a pick up, it remains significantly below historical averages. The De Novo Bank Replenishment Rate was 5.2% for L4Q, or approximately 5 new banks formed to replace every 100 lost to merger or failure. But this rate remains well below the historical average of 21.1%, or 21 new banks chartered to replace banks lost to merger or failure.

BANK FAILURE RATE:

There were no bank failures for the L4Q ending Q1 2022. Hence, the Bank Failure Rate was 0.0%.

Financially, the industry is sound. Earnings were solid. Credit quality looks good. And capital levels are strong.

2022 OUTLOOK:

Continued moderate pace with banking industry consolidation continuing near historic averages.

This will result from a below average rate of bank mergers. No reason to believe any unusual resurgence.

The bank failure rate should continue hovering at or just above zero.

And de novo bank activity will continue to be nominal in the +/- 5% range.